Cyber Threats and Attacks

View All →

Scam

View All →

Security

View All →

Latest Posts

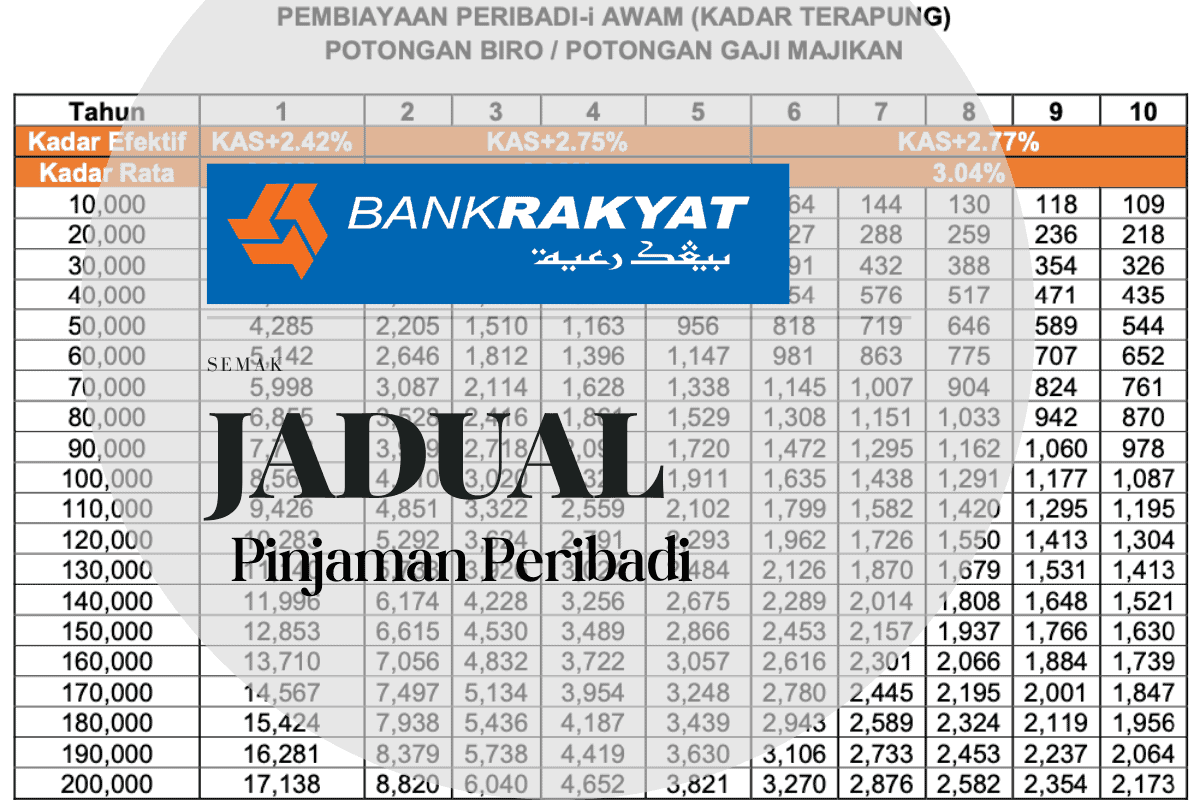

Jadual Pinjaman Peribadi Bank Rakyat 2023

Sebelum buat personal loan, sila rujuk jadual pinjaman peribadi Bank Rakyat ini dulu. Mudah untuk buat bayaran balik nanti.